Toolkit

How can sweetened beverage taxes and taxes on unhealthy food be adopted? How can sweetened beverage taxes and taxes on unhealthy food be adopted?

Build the policy rationale

Gather local evidence on the problems that taxes on sweetened beverages and foods high in nutrients and ingredients of concern (e.g., fat, salt and sugar) that are often ultra-processed are designed to address (e.g., prevalence of overweight/obesity among children and adults, evidence of household purchases or per capita sales). This will help stakeholders develop and defend an appropriate policy response, including if the policy is challenged in court.

- Types of data to collect:

- UNICEF’s Analysis Tool (Worksheets)

- P. 9 of World Cancer Research Fund International’s Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- P. 5 of Global Health Advocacy Incubator’s Research for Advocacy Action Guide Five Strategies to Use Research in a Policy Change Campaign

- Potential data sources: Annex 1 on p. 97 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

- Evidence on why sugar-sweetened beverages should be prioritized for taxation: Box 2 on p. 9 of WHO’s Action for health taxes from policy development to implementation

- Justifications for adopting sugary drink taxes: Appendix I of ChangeLab Solutions and Healthy Food America’s A Legal and Practical Guide for Designing Sugary Drink Taxes: Second Edition

Collect global evidence on why taxes are part of the solution, including their effect on prices, consumer purchasing and consumption. This should include data that demonstrates that taxes do not negatively affect the economy (e.g., wages, job loss), both to anticipate and challenge the common food and beverage industry argument that health taxes are bad for business.

- Evidence to counter the industry’s economic arguments:

- (U.S.) Healthy Food America’s Sweetened Beverage Taxes and Employment

- (Global) Global Health Advocacy Incubator’s Responses to the food and beverage industry’s economic arguments against healthy food policies

- Evidence for taxing nonsugar sweeteners: Global Health Advocacy Incubator’s Sweeteners: Potential Health Harms and Taxation

- Citable list of global mandates and action plans: P. 12 and 13 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

Data collected should explicitly show how tax policies contribute to health equity.

- Evidence on health and equity outcomes of implemented taxes:

- Food Policy Hub’s evidence page

- P. 10 of WHO’s Action for health taxes from policy development to implementation Making the case for sugar-sweetened beverages taxes

- Evidence on how subsidies can complement tax policies: Food Policy Hub’s healthy food subsidies evidence page (coming soon!)

If advocating for an amended tax policy design (e.g., rate, types of taxed products), collect data that captures current shortcomings and supports the proposed design.

Develop measurable policy objectives

Setting strong evidence-backed objectives will help:

- Ensure the policy is designed well

- Promote transparency as to why it is being introduced or amended

- Facilitate monitoring and evaluation to make sure objectives are being met

- Protect the tax from legal challenges by demonstrating it serves a legitimate public interest and is proportionate to achieve those aims

The primary objective of a tax on sweetened beverages and unhealthy foods should be health related.

Example of a strong policy objective for sweetened beverage taxes

“Decrease the consumption of all sweetened beverages ideally expressed as a specific reduction rate over a defined period, based on the country context, including those with any amount of sugar and with any amount of non-sugar sweeteners.”

For more information, see p. 13-14 of Global Health Advocacy Incubator’s position paper on sweetened beverage taxes (coming soon!)

Secondary objectives may include increasing public awareness of unhealthy foods and beverages, increasing purchases of healthy alternatives like water, raising revenue and spurring product reformulation.

- More on why reformulation may undermine public health: P. 13 of Global Health Advocacy Incubator’s position paper on sweetened beverage taxes (coming soon!)

Policy objectives should be measurable in the short term since long-term objectives like reduced diet-related chronic disease prevalence could take years to measure, potentially leading to claims that the policy did not work.

Research the policy environment

It is important to understand what other nutrition policies exist to position taxes on sweetened beverages and unhealthy food as part of a package of policies for healthier food environments and to align objectives, definitions, processes and tools such as nutrient profile models.

It is also worth investigating potential political and/or legislative opportunities where tax policies may be more easily introduced.

This may include:

- Amid tax reforms

- When there are shifts in political leadership

- When a national health and nutrition strategy is introduced or updated

- When there is increased debate on overweight and obesity and unhealthy food and drinks

- How to seize policy windows: Toolbox 1 on p. 17 and 18 in the World Health Organization’s Action for health taxes from policy development to implementation

Understand the legal context

Many countries already have excise taxes on at least one type of sweetened beverage, but these may not be designed with explicit health objectives. Therefore, it is important to review any existing excise tax laws and understand the process for amending them before introducing a sweetened beverage tax.

Advocates should focus efforts on pursuing tax reform through the proper legislative process in their country. In most countries, taxes must be created through formal legislation to comply with legal principles. Taxes implemented through budget amendments or executive orders may face legal challenges or be declared unconstitutional.

It is also crucial to understand regional or international legal frameworks relevant to taxes, including:

- International trade agreements (e.g., World Trade Organization)

- Regional trade agreements

- International investment agreements

Trade and investment agreements may present constraints but generally have exceptions that permit governments to protect public health.

- Conducting a legal analysis:

- P. 17-20 of the World Health Organization’s Action for health taxes from policy development to implementation Making the case for sugar-sweetened beverages taxes

- P. 5-8 of Global Health Advocacy Incubator’s Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

Map potential stakeholders

Political support is very important for taxes on sweetened beverages and unhealthy foods.

Key government stakeholders:

- The Ministry of Finance—An important stakeholder, since they are responsible for implementing the tax. They can provide powerful support for the policy to pass if it is positioned as aligning with their goals, such as addressing budget deficits or assuaging concerns around job loss and economic productivity.

- The Ministry of Health—A powerful champion for the tax from a health perspective, providing evidence on public health benefits and disease prevention.

Other important stakeholders to map:

- Researchers and academic institutions

- Civil society organizations

- Media outlets

Opposition to anticipate:

The food and beverage industry often presents powerful resistance, including:

- Sweetened beverage manufacturers

- Ultra-processed food producers

- Distributors

- Sugar farmers and refiners

Example interest-influence grid (Toolbox 2 on p. 21). Source: Action for health taxes from policy development to implementation. Geneva: World Health Organization and the United Nations Development Programme, 2024. Licence: CC BY-NC-SA 3.0 IGO.

- Guidance on conducting a stakeholder analysis:

- P. 7-9 of Global Health Advocacy Incubator’s Advocacy Action Guide Four Phases to Health Policy Success

- P. 9 of Global Health Advocacy Incubator’s Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

- Toolbox 2 on p. 21 of the World Health Organization’s and United Nation Development Program’s Action for health taxes from policy development to implementation

- P. 23-26 of the United Nation Development Program’s Institutional and Context Analysis for the Sustainable Development Goals

Industry Interference Examples:

- Promote disinformation via the media

- Corporate-wash and lobby to develop political allies

- Fund research claiming taxes do not work

Resources:

- ChangeLab Solutions and Healthy Food America: A Legal and Practical Guide for Designing Sugary Drink Taxes: Second Edition

- Food Policy Hub: food subsidies page (coming soon!)

- Food Policy Hub: What is the evidence for sweetened beverage taxes and taxes on unhealthy foods?

- Global Health Advocacy Incubator: Sweetened Beverage Taxes: Designing and Promoting Tax Policies with the Highest Standards Position Paper [forthcoming].

- Global Health Advocacy Incubator: Evidence on ultra-processed product taxes: evaluations and simulations (2022-2024)

- Global Health Advocacy Incubator: Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

- Global Health Advocacy Incubator: Research for Advocacy Action Guide Five Strategies to Use Research in a Policy Change Campaign

- Global Health Advocacy Incubator: Responses to the food and beverage industry’s economic arguments against healthy food policies

- Global Health Advocacy Incubator: Sweeteners: Potential Health Harms and Taxation

- Healthy Food America: Sweetened Beverage Taxes and Employment

- UNICEF: Landscape Analysis Tool and Worksheets

- United Nation Development Program: Institutional and Context Analysis for the Sustainable Development Goals

- World Cancer Research Fund International: Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- World Health Organization and United Nation Development Program: Action for health taxes from policy development to implementation

- World Health Organization and United Nations Development Program: Action for health taxes from policy development to implementation Making the Case for Sugar-Sweetened Beverage Taxes

- World Health Organization: WHO Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

The way health taxes are framed and presented is important since they tend to be less widely understood than other food policies. The food and beverage industry will likely exert heavy opposition against the policy, making it important for tax advocates to have the “winning” narrative from early on.

The framing should align with the objectives and design of the policy. Taxes can be presented as a win across multiple fronts:

- A win for public health (reducing purchases and consumption of targeted unhealthy products and preventing associated health care costs)

- A win for government revenue (increasing revenue that can be directed into social and public health programs)

- A win for health equity (addressing disproportionate diet-related disease burdens among lower-income populations, with revenue targeted toward equity-focused programs)

- A win for human rights (advancing the right to health by discouraging unhealthy consumption while generating revenue that enables governments to fulfill other rights requiring adequate funding)

- How to strategically frame the tax: P. 86-87 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

Research shows that framing the tax as a way to improve health while also raising revenue for social good, leads to higher public and political support. For subnational/local taxes, it is important to understand local context and citizen priorities to frame the tax accordingly.

Image source: “Yes on Dale” by Quinn Dombrowski / quinn.anya, adapted by Food Policy Hub. Original: https://www.flickr.com/photos/quinnanya/15460942958 © Quinn Dombrowski. Licensed under CC BY-SA 2.0. This adaptation is shared under the same license.

In Berkeley, California in the U.S. where citizens tend to be more politically active and likely to challenge big corporations, the tax was framed as “Berkeley vs. Big Soda,” a policy to improve health and raise revenue for programs for healthier living.

Resources:

- Revenue generation framing: P. 16-18 of World Cancer Research Fund International’s Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- How revenue from sugar-sweetened beverage taxes has been used: Annex 3 on p. 59 of the World Health Organization’s Global report on the use of sugar-sweetened beverage taxes 2023

- Activities funded by sugary beverage tax revenue in the U.S.: Table 4 on p. 17 of ChangeLab Solutions and Healthy Food America’s A Legal and Practical Guide for Designing Sugary Drink Taxes. For more on dedicating tax revenues, see p. 18.

- Current economic arguments for health taxes: Task Force on Fiscal Policy for Health’s Health Taxes: A Compelling Policy for the Crises of Today

Industry Interference Examples:

- Reframe issue as one of individual responsibility, blame lack of physical activity for rise in overweight and obesity and/or suggest that single product categories, such as sweetened beverages, are unfairly targeted

- Frame taxes as bad for the economy, regressive, discriminatory (placing greater burden on certain groups of people like those with lower income) and ineffective at reducing purchases and consumption

Resources:

- ChangeLab Solutions and Healthy Food America: A Legal and Practical Guide for Designing Sugary Drink Taxes

- Task Force on Fiscal Policy for Health (2024): Health Taxes: A Compelling Policy for the Crises of Today

- World Cancer Research Fund International: Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- World Health Organization: Global report on the use of sugar-sweetened beverage taxes 2023

- World Health Organization: Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

When resources are available, it is valuable to estimate the effect that a proposed tax would have on product prices, consumption and government revenues. Modeling studies can be conducted by governments internally or through partnerships with civil society and academia.

When conducting modelling studies, consider testing different tax scenarios (e.g., 30%, 40%, 50%) across various demand elasticities (such as -0.8 or -1.0) to assess potential changes in price, sales and consumption patterns—ideally broken down by socioeconomic groups—and revenue generation.

Additional analyses that could strengthen the policy case are:

- Cost-effectiveness data comparing the policy to other food policy interventions

- Economic impact assessments evaluating potential effects on relevant industries

- More information: World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets:

- Compare how much revenue countries have earned – Table 2.3 on p. 21

- Guiding questions the analyses should answer – p. 38

- Types of data that can be used for country-specific impact modeling – Table 3.3 on p. 39 and 40

Industry Interference Examples:

- Fund or promote research that argues that taxes are ineffective or produce negative outcomes

- Use flawed projections of revenue and other variables to allege the policy is not working as intended

Resources:

- World Health Organization: Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

Building strong multi-sectoral government and civil society coalitions is crucial for policy success. Coalitions should provide clear, consistent and sustained messaging on the policy rationale and be prepared to confront industry interests and lobbying. Every coalition member should be free from food and beverage industry affiliation.

Government partnerships

Experience from countries that have implemented taxes shows that engaging government departments early—especially the finance department—helps with policy alignment, coherence and political support.

Key departments to engage include:

- Health

- Finance

- Agriculture

- Trade and commerce departments/ministries

- Government’s legislative and executive branches

Civil society and academic partnerships

Civil society organizations, including nongovernmental organizations and academia, play crucial roles in supporting government efforts.

They can:

- Survey public opinion

- Build support via the media and community outreach

- Develop local evidence

- Counter industry interference

- Monitor implementation

The coalition may include:

- Economists

- Public health experts

- Medical organizations

- Consumer advocates and other relevant stakeholders.

When tax opponents in Colombia organized a hearing against a sweetened beverage tax, a coalition of Colombian civil society organizations joined forces for demonstrations to draw media attention to the issue. Translation: Our health doesn’t have a price. #nomoreinterference from the junk food industry.

Source: El Colectivo de Abogados “José Alvear Restrepo” (CAJAR) in Colombia.

- Developing civil society coalitions: The Prevention Institute’s Developing Effective Coalitions: An Eight Step Guide

- Worksheet to identify potential partners: P. 7 of Healthcare Association of New York State, Inc.’s Coalition building toolkit

- Case study with diverse coalition experiences globally: Global Health Advocacy Incubator’s Sweetened Beverage Tax

- Coalition-building for public health advocacy campaigns: Global Health Advocacy Incubator’s webinar Building Effective Coalitions for Public Health Advocacy Campaigns

Industry Interference Examples:

- Create well-funded industry coalitions and front groups with neutral-sounding names

- Deploy coordinated lobbying campaigns and media strategies promoting anti-tax messaging

Resources:

- Global Health Advocacy Incubator: Building Effective Coalitions for Public Health Advocacy Campaigns

- Global Health Advocacy Incubator: Sweetened Beverage Tax

- Healthcare Association of New York State, Inc.: Coalition building toolkit

- Prevention Institute: Developing Effective Coalitions: An Eight Step Guide

The food and beverage industry has successfully delayed, weakened or stopped tax policies in many countries. Therefore, industry interference needs to be anticipated and countered throughout the policy process. Even after implementation, persistence in countering interference and maintaining public support remain important to help pave the way for future tax increases as needed.

Recently, Big Soda has shifted its strategy toward weakening rather than outright opposing tax policies, for example, by advocating for lower tax rates or the exclusion of certain products.

Industry tactics against taxes can be organized into five categories under the acronym “SCARE”:

(S)owing doubt by discrediting science and diverting attention

The food and beverage industry may claim there’s insufficient evidence that taxes reduce consumption and fund researchers to produce skewed data disputing effectiveness. It may also try to shift focus away from its products’ role in diet-related chronic diseases.

Communication campaigns, such as this one in South Africa, can help counter industry messaging and maintain focus on the health objectives of the tax.

Source: Murukutla N, et al. Results of a Mass Media Campaign in South Africa to Promote a Sugary Drinks Tax. Nutrients. 2020. Learn more at heala.org.

- Guidance on countering these tactics:P. 71-76 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

(C)ourt and legal challenge threats

The industry may threaten or make legal challenges based on domestic or international law, arguing the tax is unconstitutional, violates due process or breaches international trade and investment commitments. These threats can create “regulatory chill,” where governments avoid implementing policies due to fear of being challenged by foreign investors. This highlights the importance of developing policies to be more likely to withstand legal challenges or threats. Having clear public health objectives that frame health taxes as legitimate disease prevention measures makes them more defensible against claims they infringe commercial or other rights.

- Guidance on countering these tactics: P. 76-78 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

- Evidence on how taxes can advance health equity: Food Policy Hub’s evidence page

(A)nti-poor rhetoric (regressivity)

The industry often argues that taxes disproportionately hurt people with lower income because they are regressive (e.g., tax burden decreases with income). It is important to address this concern while conveying that because lower-income populations are more responsive to taxes and bear a disproportionate burden of diet-related diseases, they experience greater health benefits and larger reductions in health-related costs. While taxes can be progressive in health terms even without additional measures, pairing them with subsidies on healthier food or using revenue to support health equity initiatives, including access to healthy food, can further help defend against this argument.

- Guidance on countering these tactics: P. 78-79 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

- Evidence on how taxes can advance health equity: See Food Policy Hub’s evidence page

(R)evenue instability

The industry may claim taxes will not meet revenue projections or use flawed projections to build opposition. Projecting revenue as accurately as possible and being clear about the tax’s objective and indicators of success will help withstand these arguments.

- Guidance on countering these tactics: P. 79-80 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

(E)mployment impact

The industry will often claim that taxes negatively affect employment (manufacturing, crop agriculture) and reduce foreign investment, along with other negative effects on the economy. However, these arguments often rely on faulty research methods and do not account for the longer-term benefits of improved population health. Public health evidence has repeatedly demonstrated no job loss and even shows gains from jobs shifting to other sectors and from government expenditure of tax revenue.

- Guidance on countering these tactics: P. 80-81 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

- Evidence to counter the industry’s economic arguments (U.S.): Healthy Food America’s Sweetened Beverage Taxes and Employment

- Common arguments from opponents and counterarguments according to the SCARE paradigm: Table 1 on p. 12-14 of the World Health Organization’s Fiscal Policies to Promote Healthy Diets: Policy Brief

- Common industry arguments and counterarguments:

- Global Health Advocacy Incubator and Global Food Research Program at UNC-Chapel Hill’s Sugar-Sweetened Beverage Taxation – Industry Arguments

- World Banks’ Countering Common Arguments Against Taxes on Sugary Drinks

- P. 19-23 of World Cancer Research Fund International’s Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- P. 10 of Vital Strategies, Economics for Health and REEP’s The Future of Health Financing in Africa: The Role of Health Taxes

- Examples of industry interference in sweetened beverage tax policies worldwide: Global Health Advocacy Incubator’s Sweetened Profits: The Industry’s Playbook to Fight Sweetened Beverage Taxes. For recommendations to strengthen and protect tax policies see p. 32-34.

Resources:

- Food Policy Hub: What is the evidence for sweetened beverage taxes and taxes on unhealthy foods?

- Global Health Advocacy Incubator and Global Food Research Program at UNC-Chapel Hill: Sugar-Sweetened Beverage Taxation – Industry Arguments

- Global Health Advocacy Incubator: Sweetened Profits: The Industry’s Playbook to Fight Sweetened Beverage Taxes

- Healthy Food America: Sweetened Beverage Taxes and Employment

- World Bank: Countering Common Arguments Against Taxes on Sugary Drinks

- World Cancer Research Fund International: Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- World Health Organization: Fiscal Policies to Promote Healthy Diets: Policy Brief

- World Health Organization: Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

Civil society can lead advocacy efforts to build stakeholder support from politicians, academia and the public, making sure that policy messaging is clear and consistent throughout the process.

Understanding public opinion

Public opinion is often used by both pro- and anti-tax sides to sway policymakers, which makes registering public values and preferences an important basis for tax policies. This information can help create appropriate campaign messaging and a better understanding of how the public may interact with the tax once it is implemented.

Methods to engage public opinion:

- Opinion polls

- Discrete-choice experiments

- Other survey approaches

Building public and policymaker support

Awareness campaigns: Public awareness campaigns can be used to raise awareness on the need for taxes and can be targeted toward decision-makers at key decision moments. Using earned media helps retain control over the narrative and expose industry counter-efforts.

Community engagement: Working with affected communities—especially those experiencing health inequities related to sweetened beverages or unhealthy food—can help build a policy that is equitable and responsive to those it affects the most.

- Guide to public health communication and media advocacy: Global Health Advocacy Incubator’s Communications & Media Advocacy Action Guide

- Communication and media strategies: P. 21-22 of Action for Healthy Food’s A Roadmap for Successful Sugary Drink Tax Campaigns

- Community engagement strategies: P. 11 of ChangeLab Solutions’ Sugary Drink Strategy Playbook Reducing Sugary Drinks to Promote Community Health and Equity

Managing conflict of interest

It is crucial that potential conflicts of interest are carefully managed when industry stakeholders are involved in the policymaking process. WHO and leading academics recommend that governments put safeguards in place to manage and prevent conflicts of interest and improve transparency. When industry consultation occurs, it should ideally be through public hearings that include independent experts and civil society to provide balance and oversight.

Industry Interference Examples:

- Launch campaigns against the tax to “win” public opinion

- Lobby politicians against policy adoption

Resources:

- Action for Healthy Food: A Roadmap for Successful Sugary Drink Tax Campaigns

- ChangeLab Solutions: SUGARY DRINK STRATEGY PLAYBOOK Reducing Sugary Drinks to Promote Community Health and Equity.

- Global Health Advocacy Incubator: Communications & Media Advocacy Action Guide

Taxes should be passed to consumers in the form of higher prices that are noticeable in retail environments, leading to reduced purchases.

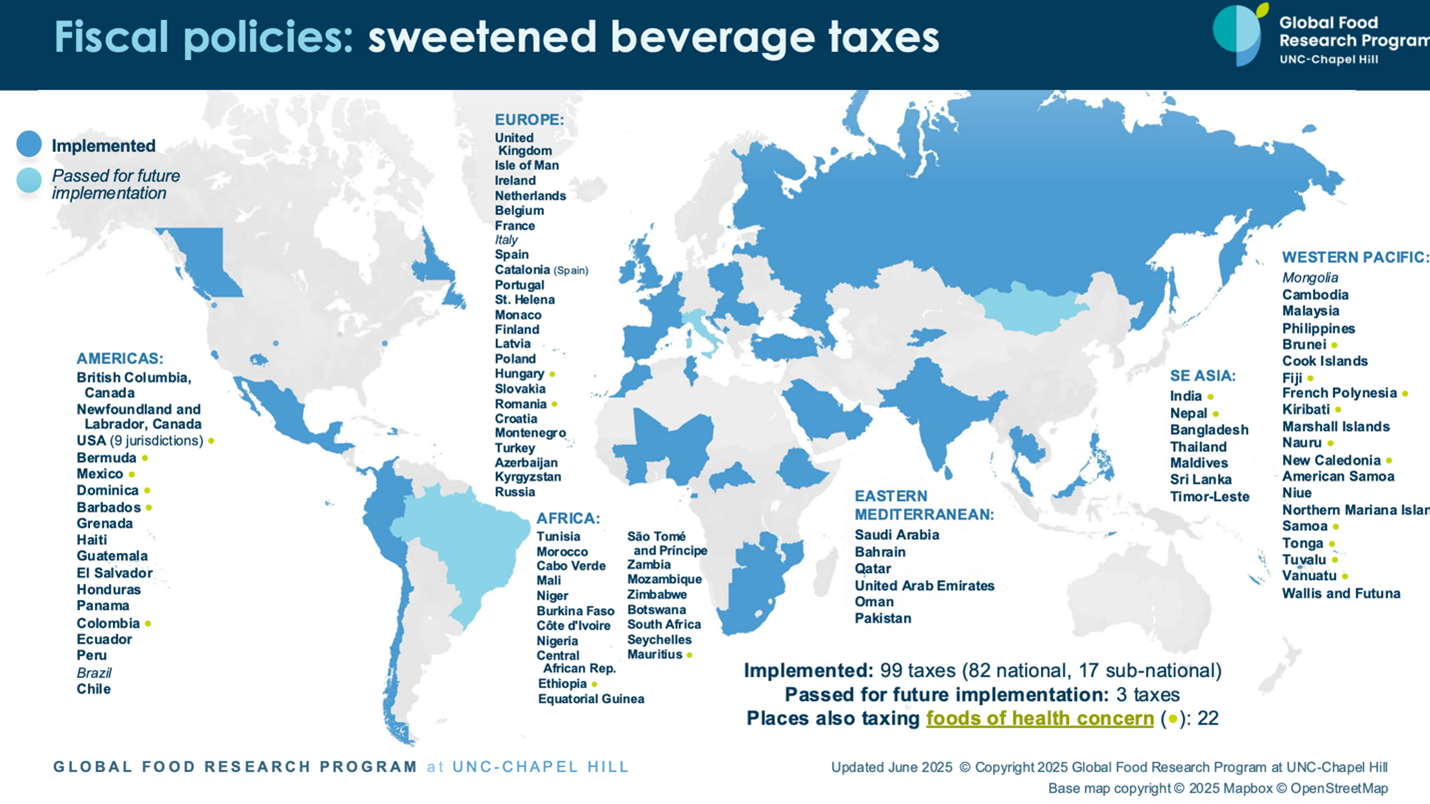

99 countries and smaller jurisdictions tax sweetened beverages- 82 national

- 17 subnational

Source

Global Food Research Program at UNC-Chapel Hill. Maps: Food and beverage taxes. 2025 June.

Note: These counts are lower than the World Health Organization’s because they exclude countries that tax plain package water at a similar rate to sweetened beverages.

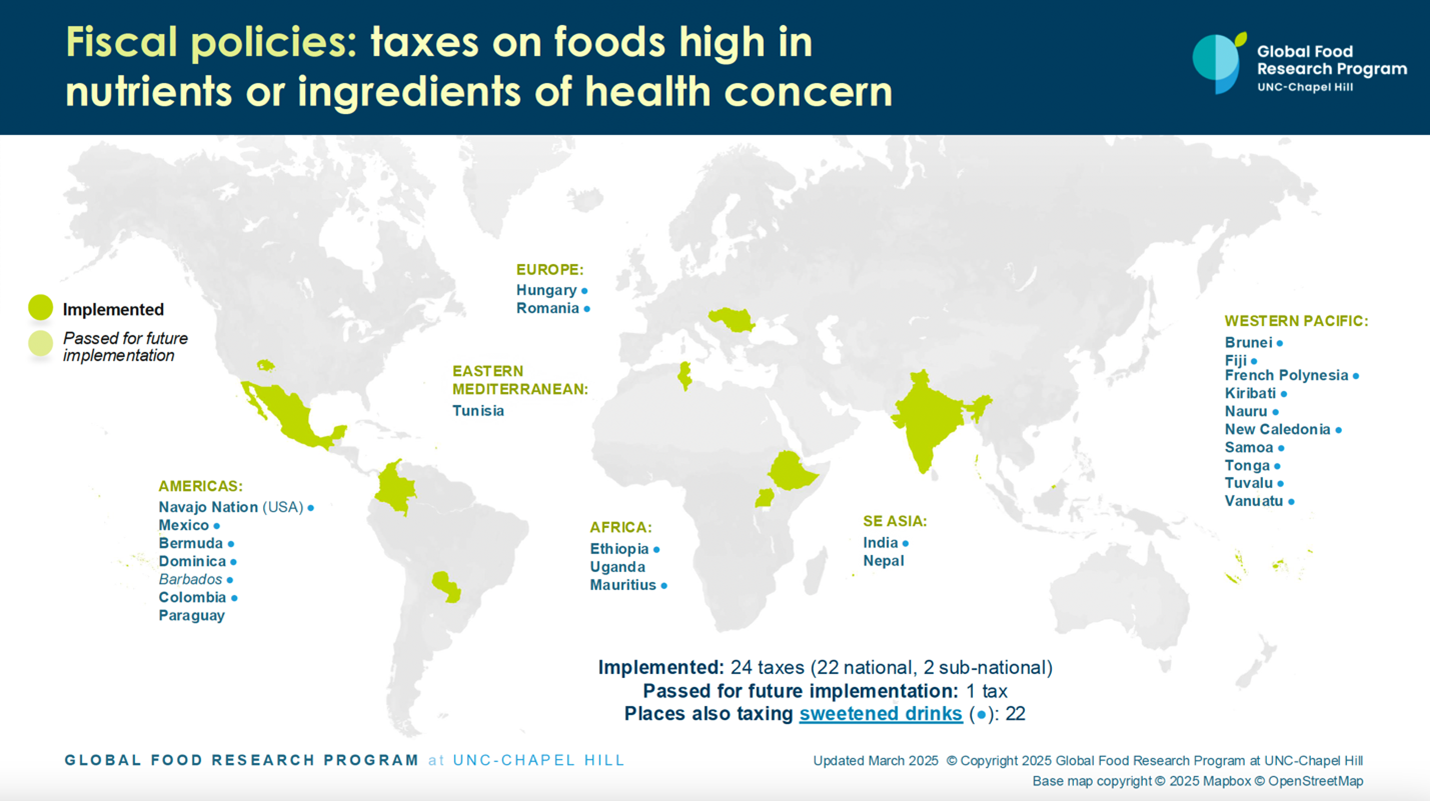

24 tax foods or ingredients high in nutrients of concern- 22 national

- 2 subnational

Source

Global Food Research Program at UNC-Chapel Hill. Maps: Food and beverage taxes. 2025 June.

Visit the Global Food Research Program at UNC-Chapel Hill’s website for these and other maps.

Key recommendations for sweetened beverage tax design*

- Use specific excise taxes based on volume

- Apply to all beverages containing sugar or sweetener (whether added or intrinsic)

- Be high enough to significantly reduce consumption. Research indicates that taxes that raise prices by 50% or higher can achieve the greatest health benefits.

For more information, view Global Health Advocacy Incubator’s position paper on Sweetened Beverage Taxes (coming soon!)

*Many lessons from sweetened beverage taxes are transferable to unhealthy food taxes, though evidence is still emerging.

Tax type and base

For public health benefits, excise taxes are preferred over other types of taxes because they apply to specific products in retail environments and increase their prices relative to other products.

Excise taxes can be:

- Uniform—the same tax type and rate apply to all taxable products

- Tiered—the tax rate varies according to product characteristic (e.g., sugar content, type of beverage)

Excise taxes can take three forms:

- Ad valorem—levied as a percentage of the product value

- Specific—monetary value associated with a physical characteristic of the product, including nutrient content (e.g., sugar content), volume (e.g., per liter) or a hybrid of both (tiered taxes by nutrient content and volume)

- Mixed—combination of ad valorem and specific excise taxes

From a public health perspective, specific excise taxes are more effective than ad valorem taxes because they target cheaper products and are less susceptible to price manipulation. However, they require regular inflation adjustments—ideally annual—to maintain effectiveness.

The tax base should depend on the policy objective. However, for sweetened beverages, recent evidence shows that reducing the total volume of any consumed beverages may be most strategic to achieve long-term consumption changes and health benefits.

- More on tax type and base: P. 15-20 of Global Health Advocacy Incubator’s Position Paper Sweetened Beverage Taxes (coming soon!)

- Comparison of tax designs: Table 4.1 on p. 57-58 of the World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthier Diets

Taxable products

Taxes may be levied on:

- All products of a certain type (e.g., nonalcoholic beverages with added or intrinsic sweetener)

- Products based on nutrient content (e.g., 4g or more of added sugar per 100ml)

For sweetened beverages, the preferred approach is taxing all beverages containing added sugar or nonsugar sweetener—including concentrated or powdered forms—to prevent substitution to untaxed unhealthy alternatives and to signal that products are being taxed because they are not essential to people’s diets. Nonsweetened bottled water should be excluded from the tax. Ideally, taxable products should be based on evidence-based guidelines, such as nutrient profile models.

- More information on nutrient profile models: Global health Advocacy Incubator’s Nutrient Profile Models Position Paper

Tax implementation should include messaging about healthier food and beverage alternatives. In areas lacking safe drinking water, improving access should be prioritized alongside the tax.

- More on policy scope: P. 14-15 of Global Health Advocacy Incubator’s Position Paper on Sweetened Beverage Taxes (coming soon!)

Tax rate

Most taxes implemented to date have raised prices on sweetened beverages by relatively little (<10%). Low rates may produce undetectable changes, fail to keep up with income growth and lead to claims the tax didn’t work. There is also the risk that incomplete pass through of the price to the consumer due to poorly designed policies or industry responses to policies, lowers effectiveness.

- Estimated tax pass-through rates in various countries: Figure 1 on p. 12 in the Task Force on Fiscal Policy for Health’s Using Fiscal Policy to Promote Health: A Five-Year Update on Taxing Tobacco, Alcohol and Sugar-Sweetened Beverages

Economic theory and evidence to date, suggests that larger taxes lead to bigger changes in consumption due to increased prices and more awareness of health harms. Increasing the tax outright, rather than in small, incremental increases over time, has a bigger effect on consumption.

Recent research on sweetened beverage taxes indicates that taxes raising prices by 50% or higher can achieve the greatest health benefits. This has led WHO to recommend that countries implement such taxes, while acknowledging that each country should evaluate what best fits its context.

- More on tax rate: P. 20-21 of Global Health Advocacy Incubator’s Position Paper on Sweetened Beverage Taxes. For sweetened beverage tax examples, see Appendix 3 on p. 33-35. (coming soon!)

Tax revenue and earmarking

Earmarking allows governments to designate tax revenues for specific programs or purposes. It is important to first assess legal feasibility for earmarking tax revenue, as restrictions vary by jurisdiction. Where earmarking is legally possible, revenue should support public health and health equity goals.

Hard earmarking designates legislated, fixed amounts of revenue for a specific purpose, not subject to annual budget review

Soft earmarking notionally links revenue to a health goal while keeping actual allocations flexible and decided through the normal budget process based on population needs

Examples of how tax revenue has been used:

Philippines—Sweetened beverage tax funding universal health care:

50% of revenues from The Philippines’ ₱6 (US~$0.10) per liter sweetened beverage tax is soft-earmarked for health, funding PhilHealth (Universal Health Care), medical assistance and health facility upgrades.

Mexico—Sweetened beverage tax revenue directed to health and water access:

In Mexico, the law states that revenue should be allocated to programs for the promotion, prevention, detection, treatment and control of malnutrition, overweight, obesity and diet-related chronic diseases, as well as increasing access to potable water in rural areas and schools with lower educational outcomes. However, Mexico did not formally earmark tax revenue, and the extent to which revenues are directed toward these stated purposes—particularly water fountains in schools has remained unclear in practice.

- More on revenue usage and earmarking, including global examples: P. 22-23 of Global Health Advocacy Incubator’s Position Paper on Sweetened Beverage Taxes

- Information on equitable revenue allocation: Healthy Food America and The Praxis Project’s Equitable Sugary Drink Tax Policy Recommendations

Legal considerations

To be in the strongest position to withstand legal challenges, the policy needs to be carefully developed in consultation with legal experts. This includes being nondiscriminatory—or applying equally to similar imported and locally manufactured products, as is the case for excise taxes—and carefully designing key legal elements such as tax structure, covered products and implementation mechanisms.

- Guide to legal drafting: P. 12-24 of Global Health Advocacy Incubator’s Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

- List of legal considerations: P. 20 of the World Health Organization’s Action for health taxes from policy development to implementation Making the case for sugar-sweetened beverages taxes

- Measures that could complement sweetened beverage taxes: ChangeLab Solutions’ SUGARY DRINK STRATEGY PLAYBOOK Reducing Sugary Drinks to Promote Community Health and Equity

Industry interference Examples:

- Propose weaker taxes (e.g., lower tax rate, exclusion of certain products) or alternatives to taxes

- Threaten or take legal action

- Stigmatize tax using economic and other arguments in the media and when lobbying policymakers

Resources:

- ChangeLab Solutions: SUGARY DRINK STRATEGY PLAYBOOK Reducing Sugary Drinks to Promote Community Health and Equity

- Global Food Research Program at UNC-Chapel Hill: Food and Beverage Taxes Global Maps

- Global Health Advocacy Incubator: Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

- Global Health Advocacy Incubator: Position Paper Nutrient Profile Models A Valuable Tool for Developing Healthy Food Policies

- Global Health Advocacy Incubator: Sweetened Beverage Taxes: Designing and Promoting Tax Policies with the Highest Standards Position Paper (coming soon!)

- Healthy Food America and The Praxis Project: Equitable Sugary Drink Tax Policy Recommendations

- Task Force on Fiscal Policy for Health: Using Fiscal Policy to Promote Health: A Five-Year Update on Taxing Tobacco, Alcohol and Sugar-Sweetened Beverages

- World Health Organization: Action for health taxes from policy development to implementation Making the case for sugar-sweetened beverages taxes

- World Health Organization: Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthier Diets

Implementation should be considered from the early policy stages. A monitoring and evaluation framework should be developed alongside the tax’s introduction that assigns responsibilities for monitoring, enforcing compliance and sanctioning violations. Tax revenue can fund these efforts.

- Learn more: P. 20 of Global Health Advocacy Incubator’s Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

Monitor implementation

Implementation success can be affected by responses from industry, consumers, policymakers and the market. Monitoring helps ensure the tax achieves its impact, identifies loopholes, offers opportunities to improve or expand the tax (e.g., higher tax rate) and provides for more accurate evaluations. A government agency or independent group free of conflicts of interest should coordinate monitoring with academia and civil society.

Enforce implementation

Include sanctions, penalties or other enforcement measures for noncompliance. Many of the compliance concerns around health taxes are like those of other excise taxes.

- More on compliance: World Health Organization’s Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

- Key stages of compliance with taxes – p. 63-65

- Strategies to minimize noncompliance – p. 65

Determine revenue allocation with local communities

If funds are being earmarked in local jurisdictions, a community advisory board composed of people from affected communities and experts can guide resource allocation and monitoring. Annual public reports detailing revenue collection and spending can help ensure transparency and accountability.

- More on community advisory boards: P. 19 of ChangeLab Solutions and Healthy Food America’s A Legal and Practical Guide for Designing Sugary Drink Taxes. For model language for the creation of a community advisory board, see Appendix 2 on p. 34-35.

Conduct community outreach and education initiatives

Activities should reach:

- Distributors and retailers paying the tax.

- Advocates and partners who supported the tax—they remain crucial for conducting local education initiatives and defending against industry interference during implementation.

- The public, especially communities most affected by diet-related health issues, to explain the tax’s purpose, benefits, timeline, revenue use and impacts.

- Examples of communication materials supporting local tax administration in the U.S.:

- Philadelphia’s Payments, assistance and taxes webpage

- Seattle’s Sweetened Beverage Tax webpage

Industry Interference Examples:

- Take or threaten legal action based on domestic or international law

- Lobby to pressure reversal

- Conduct marketing strategies to undermine tax (price promotions, changing size of products)

Resources:

- ChangeLab Solutions and Healthy Food America: A Legal and Practical Guide for Designing Sugary Drink Taxes

- Global Health Advocacy Incubator: Legal Advocacy Action Guide Legal Strategies for Public Health and Industry Accountability

- Global Health Advocacy Incubator: Sweetened Beverage Taxes: Designing and Promoting Tax Policies with the Highest Standards Position Paper

- World Health Organization: Manual on Sugar-Sweetened Beverage Taxation Policies to Promote Healthy Diets

After introducing a tax policy, evaluate:

- Whether the policy is being executed as intended

- Effectiveness in achieving policy objectives

- Impact on longer-term goals

Why evaluation matters

Evaluation data supports other countries implementing similar policies by demonstrating successes and identifying improvement opportunities. Robust data collection strengthens the evidence base for effective tax policy design, helping policymakers make informed decisions.

Key evaluation principles

- Establish baselines by collecting pre-tax purchase and consumption data

- Ensure independence through conflict-of-interest-free evaluations

- Create oversight—some countries use independent advisory committees

- Promote transparency by making data public and sharing results through media

- Break down analyses by sex, gender, geography, and especially socioeconomic status to allow researchers to assess impacts on health equity

- Core principles for evaluating sugar-sweetened beverage taxes: Appendix on p. 28 in World Cancer Research Fund International’s Building momentum: lessons on implementing a robust sugar sweetened beverage tax

Evaluations may measure:

1. Is the tax working as intended? (Process evaluation)

- Clear guidance on tax collection (who pays, when, which products)

- Defined penalties for noncompliance

- Transparent revenue use

- Clear departmental responsibilities for implementation

2. Is the tax meeting objectives? (Outcome evaluation)

- Product price changes

- Sales changes for targeted products

- Consumption changes for targeted nutrients of concern

3. Is the tax achieving longer-term goals? (Impact evaluation)

- Policy cost savings

- Employment and revenue impacts

- Diet-related chronic disease rates

Natural experiment approaches and long-term modeling

The following natural experiment methods are generally recommended to measure tax impacts:

- Interrupted time series: Compare data before and after tax implementation

- Difference-in-difference: Compare exposed vs. unexposed populations before and after the tax

- Examples of how these methods have been used: Table 2 of Ng, et al.’s How should we evaluate sweetened beverage tax policies? A review of worldwide experience

Long-term health outcomes require simulation modeling combined with real-world data. For example, researchers may combine actual changes in sweetened beverage purchases with mathematical models of disease development.

Note: Changes in chronic disease rates take years to appear and cannot be fully attributed to one policy alone. Research plans should set clear expectations with stakeholders about what is measurable and achievable within realistic timelines.

- Examples of how these methods have been used: Table 3 of Ng et al.’s How should we evaluate sweetened beverage tax policies? A review of worldwide experience

- Best practices to evaluate sweetened beverage taxes: Ng et al.’s How should we evaluate sweetened beverage tax policies? A review of worldwide experience

- Review methodologies for economic evaluations of sugar-sweetened beverage taxes: Thiboonboon et al.’s Economic Evaluations of Obesity-Targeted Sugar-Sweetened Beverage (SSB) Taxes–A Review to Identify Methodological Issues

Industry interference Example:

- Fund evaluation research to assert the policy is ineffective and causes economic harms

Resources:

- World Cancer Research Fund International: Building momentum: lessons on implementing a robust sugar sweetened beverage tax

- Ng et al.: How should we evaluate sweetened beverage tax policies? A review of worldwide experience

- Thiboonboon et al.: Economic Evaluations of Obesity-Targeted Sugar-Sweetened Beverage (SSB) Taxes–A Review to Identify Methodological Issues